TL;DR

Shelter saves you money by turning financial surprises into earlier decisions. It forecasts the next 30 days, shows what is actually safe to spend, catches bill collisions, surfaces recurring charges, warns about low-balance risk, and helps you decide when to hold back, cancel, move a due date, or protect cash for something more important.

Most money leaks do not feel dramatic while they are happening.

They look like a subscription you forgot to cancel, a bill that lands two days before payday, a debit card purchase made from an account balance that looked safe, or an extra debt payment that felt responsible until rent and utilities posted in the same week.

That is the problem Shelter is built around. A raw bank balance tells you what is in the account right now. It does not tell you what is already spoken for. It does not tell you whether you will hit a low point next Tuesday. It does not tell you whether the $74 you are about to spend is harmless or the beginning of a tight week.

Shelter saves you money by making that near future visible before it becomes expensive.

It does not save money by forcing you into a perfect budget. It does not shame every purchase. It does not move your money, cancel subscriptions for you, or negotiate bills behind your back. Shelter is read-only by design. Its job is to show you what is coming, what is safe, what is risky, and which small move would protect your next few days.

That sounds simple. In practice, it changes a lot.

The Break-Even Math Is Smaller Than You Think

Shelter is a paid app. Current pricing is $9.99 per month or $79 per year.

That means Shelter does not need to create some huge financial transformation to be worth it. The break-even point can be small:

- cancel one unused $11 monthly subscription,

- avoid one overdraft or NSF fee,

- catch one bill increase before it becomes normal,

- delay one purchase that would have forced a fee,

- move one due date so your account stops going negative between paychecks,

- or avoid one interest-heavy credit card decision because you saw the cash-flow effect first.

The important part is that Shelter does not "save" money in the abstract. It helps you find specific moments where money was about to leak out, then gives you enough context to make a better decision.

Here is the practical version:

| Money leak | What Shelter shows | The move it helps you make |

|---|---|---|

| A forgotten subscription | A recurring charge and its monthly/yearly cost | Cancel, downgrade, or keep intentionally |

| A bill cluster before payday | Your projected low-balance day | Move a due date, delay spending, or preserve cash |

| A risky purchase | What is actually safe to spend | Buy now, wait, or choose a smaller option |

| An extra debt payment | Whether it creates a shortfall this week | Pay extra only when the next bills stay protected |

| A surprise low balance | The forecast before the balance drops | Act early instead of reacting after a fee |

Shelter is useful when one or two of those moments happen every month. For many people, they do.

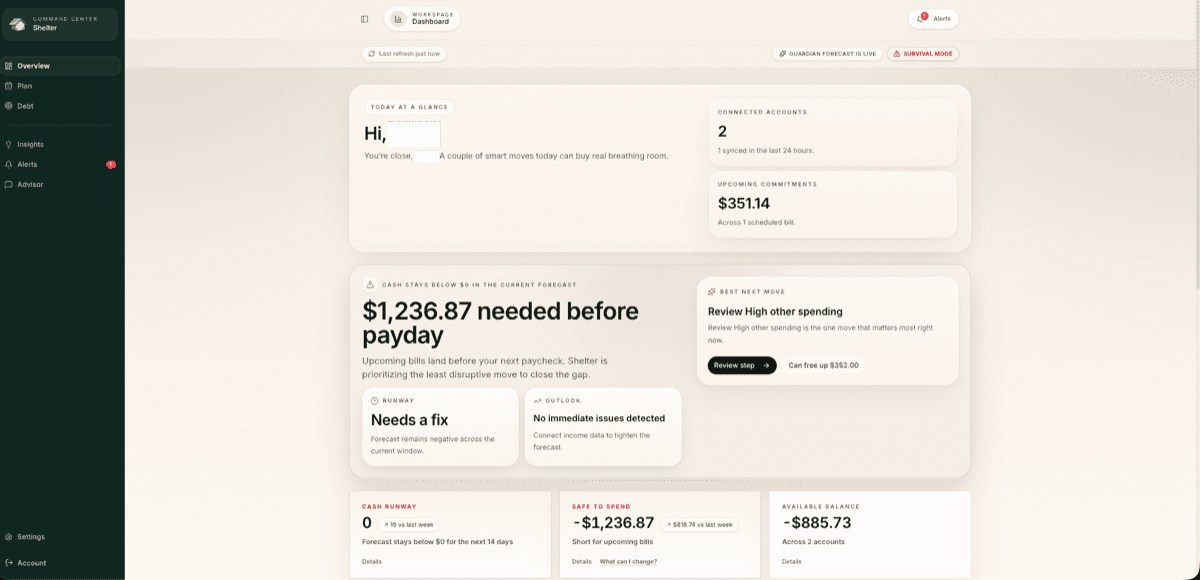

1. Shelter Replaces Guesswork With Safe-to-Spend

The simplest way Shelter saves money is by answering the question people actually ask before spending:

"Can I afford this without making next week harder?"

Your bank balance cannot answer that. If your checking account says $642, that number might feel comfortable. But if $480 in bills, subscriptions, and debt payments are due before your next paycheck, the real spending room is much smaller.

That difference is the whole point of safe to spend.

Shelter looks at your balance, recurring bills, expected income, subscriptions, and near-term cash pressure. Then it gives you a more honest number: what appears safe to use without putting upcoming obligations at risk.

That can save money in a few ways:

- You avoid spending from money that already has a job.

- You stop making decisions from a falsely high balance.

- You notice when a normal purchase would create a tight window.

- You can hold back earlier, while you still have options.

The savings often come from purchases you do not make at the wrong time. That does not mean you never buy the thing. It means you buy it when the forecast says it will not hurt you.

If you want the product version of this idea, the safe-to-spend app page shows how Shelter frames that number.

2. Shelter Helps Prevent Overdraft and NSF Fees

Overdraft fees usually happen because of timing, not ignorance.

People often know they have bills. They know payday is coming. They know their balance is not huge. What they do not know is the exact collision point: the day when a bill, subscription, card payment, or delayed transaction lands before the next deposit clears.

Shelter's cash flow forecast is built to catch that collision early.

Instead of waiting until your balance is already low, Shelter projects the next 30 days. It shows where your account is likely to dip, which bills are creating pressure, and whether a specific week needs extra caution.

That lead time is where the savings live.

If you see a shortfall three or four days ahead of time, you can still do something:

- pause non-essential spending,

- move money from another account,

- ask a biller to shift a payment date,

- postpone an optional purchase,

- change when you make an extra debt payment,

- or make sure a deposit clears before a transfer or autopay runs.

Those moves are boring. They are also powerful. A fee you prevent is money you keep.

Shelter's overdraft protection content goes deeper on this, but the core idea is simple: a low-balance alert after the fact is useful; a forecast before the fact is better.

3. Shelter Finds Subscription Waste

Subscriptions are one of the easiest places to lose money because they are designed to disappear into the background.

A $6.99 app. A $14.99 streaming service. A $29 software plan. A free trial that converted. A duplicate tool you forgot you had. None of those charges feels catastrophic by itself. Together, they quietly shrink your cash flow every month.

Shelter surfaces recurring charges so you can see what is still pulling money from your account.

The important distinction: Shelter does not cancel subscriptions for you. It is read-only. That is intentional. It shows the charge, the pattern, and the cost. You decide what to keep, cancel, downgrade, or replace.

This still saves money because visibility changes behavior.

When a subscription is hidden, it renews by default. When it is visible, it has to earn its place. If you cancel one unused subscription that costs more than Shelter's monthly price, the app has paid for itself for that month.

For a focused walkthrough, read how to do a subscription audit. If you are comparing tools, the best subscription tracker app page explains what to look for.

4. Shelter Catches Bill Timing Problems

Sometimes your monthly income is technically enough, but the month still feels impossible because all the bills hit in the same window.

This is not a budgeting failure. It is a timing problem.

Imagine this:

- paycheck on Friday,

- rent on Monday,

- insurance on Tuesday,

- phone bill on Wednesday,

- credit card minimum on Thursday,

- groceries somewhere in the middle,

- and the next paycheck more than a week away.

On paper, the month might work. In real life, that week can wreck you.

Shelter helps by showing the shape of the month, not just the total. It identifies upcoming bills, recurring charges, and balance pressure so you can see when several obligations are stacking up.

That gives you options:

- ask the phone company to move the due date,

- shift a credit card payment away from rent week,

- plan groceries before the tight stretch,

- avoid a discretionary purchase until after the cluster,

- or keep a small buffer in checking during the risky week.

Changing the timing of one bill does not reduce the bill itself. But it can prevent fees, stress spending, late payments, and short-term credit card reliance. That is real money.

For more on this style of planning, the bill tracker app and paycheck planning app pages explain how Shelter thinks about due dates and payday runway.

5. Shelter Makes "Can I Afford This?" Less Emotional

Money decisions get expensive when they happen under uncertainty.

If you are anxious, you may say no to everything and burn out. If you are tired of feeling restricted, you may say yes too often and deal with the consequences later. Both reactions are understandable. Neither is a good financial system.

Shelter gives you a calmer middle ground.

Instead of asking, "Do I deserve this?" or "Am I bad with money?" you can ask:

"What happens to the next 30 days if I spend this now?"

That question is less loaded. It turns a vague emotional decision into a practical tradeoff.

Sometimes Shelter will show that you are fine. Spend the money. Enjoy it without doing mental math in the checkout line.

Sometimes it will show that the purchase is technically possible but creates a tight low point before payday. That does not mean you are forbidden from buying it. It means you know the tradeoff before you make it.

This can save money by reducing impulse spending, but it can also improve your quality of life. You are not guessing from guilt. You are deciding from evidence.

6. Shelter Helps You Avoid Expensive "Responsible" Mistakes

Not every costly money decision looks irresponsible.

Sometimes the expensive move is the one that sounds disciplined:

- paying extra toward debt,

- moving too much into savings,

- making a large annual payment,

- transferring cash away from checking,

- or aggressively catching up on a bill before checking the rest of the week.

Those can be good moves. But if they create a shortfall before payday, they can backfire.

This is where cash-flow visibility matters. Shelter can help you see whether a responsible move is safe right now or better delayed by a few days.

For example, an extra $150 debt payment might save interest over time. But if making it today causes a checking shortfall when utilities post on Thursday, the immediate fee or credit card fallback can erase the benefit.

The better move might be:

- make the minimum today,

- wait until the paycheck clears,

- then send the extra payment once the next bills are protected.

That is not procrastination. That is sequencing.

Shelter's debt payoff app positioning is built around this kind of tradeoff: paying debt down matters, but keeping the current month stable matters too.

7. Shelter Is Especially Useful for Irregular Income

Traditional budgets assume the month is predictable. Many people's lives are not.

Freelancers, hourly workers, tipped workers, gig workers, contractors, students, and people with variable schedules often have income that changes from week to week. A fixed category budget can look neat on the first of the month and become useless by the tenth.

Shelter saves money here by focusing on runway instead of rigid categories.

The question becomes:

"Given what has actually landed and what is still coming due, how far does this money carry me?"

That is more useful than pretending every month is identical.

During a strong week, Shelter can help you see where extra cash can safely go: savings, debt, or a buffer. During a weaker week, it can help you identify the purchases or payments that need to wait.

That kind of timing awareness helps prevent the classic irregular-income trap: spending like a strong week will continue, then scrambling when the next deposit is lower.

If your income is variable, the budgeting app for irregular income page goes into this problem more directly.

8. Shelter Reduces the Cost of Manual Budget Burnout

A lot of people already know what they "should" do.

They should categorize every transaction. They should reconcile every account. They should review spending weekly. They should make a budget and stick to it.

But the system only works if they keep doing all of that. Many people do not. Not because they are lazy, but because the maintenance cost is high and life is already full.

Manual budgeting has a hidden failure mode: once you fall behind, the whole system gets easier to abandon.

Shelter takes a different approach. It uses connected account activity to build a forward-looking picture. You are not asked to manually enter every coffee, split every purchase, or maintain a perfect set of categories.

That can save money because the system keeps working when your attention is limited.

You still make the decisions. Shelter just does more of the watching, pattern-finding, and early warning. For people who hate budgeting, that is often the difference between having a money system and having no system at all.

If that sounds like you, read how to manage money without a budget or compare Shelter with a manual budgeting tool on the YNAB alternative page.

9. Guardian Turns the Forecast Into Action

Information only saves money if it changes what you do next.

That is where Guardian fits in. Guardian is Shelter's AI financial coach. It looks at the same reality Shelter is tracking: upcoming bills, spending patterns, low-balance risk, recurring charges, and the next few decisions that matter.

Instead of giving generic advice like "spend less," Guardian can help translate the forecast into practical next steps:

- "Hold off on non-essential spending until Friday."

- "This bill cluster is the pressure point this week."

- "Cancel or review these recurring charges."

- "Do not send the extra debt payment until the paycheck clears."

- "Your safe-to-spend number is lower than your balance because rent is already spoken for."

The value is not that an AI coach magically fixes your finances. The value is that it keeps connecting the numbers to decisions.

Most people do not need more vague financial wisdom. They need to know what to do today.

10. Shelter Saves Money by Protecting Your Attention

There is another kind of savings that is harder to measure but still real: fewer financial surprises consuming your day.

When you do not trust your balance, you check it constantly. You replay upcoming bills in your head. You wonder if a purchase was a mistake. You open your banking app before and after every payment. You carry a low-grade mental spreadsheet everywhere.

That attention has a cost.

Shelter cannot remove every money worry. But it can reduce the number of things you have to hold in memory. Bills, subscriptions, payday timing, and balance pressure are easier to manage when they are visible in one place.

That matters because exhausted people make expensive decisions. They forget renewals. They miss due dates. They stress-buy convenience. They avoid looking at their accounts until the problem is bigger.

A clearer system does not just save money by catching line items. It saves money by reducing the mental load that causes avoidable mistakes.

What Shelter Does Not Do

A thorough answer should be honest about the limits.

Shelter does not guarantee savings. It cannot control your income, bank timing, biller policies, merchant refunds, or the choices you make after seeing the forecast.

Shelter also does not:

- move money between accounts,

- make payments,

- cancel subscriptions,

- negotiate bills,

- sell your data,

- show third-party ads,

- or replace a human financial advisor for complex planning, taxes, legal issues, or investment advice.

Those limits are part of the product philosophy. Shelter is designed to be a read-only financial protection system. It gives you visibility, warnings, forecasts, and decision support. You stay in control.

A Practical 30-Day Shelter Savings Plan

If you want to use Shelter specifically to save money, do not start with a huge financial overhaul. Start with the first month.

Day 1: Connect and Find Your Real Safe-to-Spend Number

Look at the difference between your bank balance and your safe-to-spend number. That gap is the money that may already be spoken for by upcoming obligations.

If the gap surprises you, that is the first win. Shelter has already found hidden pressure.

Days 2-3: Review Upcoming Low Points

Open the forecast and identify the lowest projected balance in the next 30 days.

Ask:

- What causes that low point?

- Which bills or subscriptions hit before it?

- Does a paycheck arrive too late to help?

- Is there a discretionary purchase that should wait?

You are not trying to optimize the whole month. You are protecting the riskiest day first.

Days 4-7: Audit Recurring Charges

Review subscriptions and recurring payments. Cancel or downgrade anything that no longer earns its place.

Even one small cancellation can matter because the savings repeat every month.

Week 2: Fix One Timing Problem

Pick the bill that creates the most pressure and see whether the due date can move.

Many providers let you change billing dates. If rent hits at the start of the month, moving a phone bill or insurance payment to the middle of the month can smooth the pressure without changing your income.

Week 3: Use Shelter Before Spending

Before a non-essential purchase, check the forecast first.

You are not asking Shelter for permission. You are asking it to show the tradeoff. If the next bills stay protected, spend with more confidence. If the purchase creates pressure, wait.

Week 4: Lock In One Repeatable Rule

Choose one rule you can keep:

- "If safe-to-spend is below $100, no discretionary spending."

- "If the forecast shows a low point before payday, pause takeout."

- "If a subscription goes unused for 30 days, cancel it."

- "If extra debt payments create a shortfall, wait until after payday."

One repeatable rule beats ten ambitious rules you abandon.

The Real Way Shelter Saves You Money

Shelter saves money by changing the moment when you find out.

Without Shelter, you may find out after the fee posts, after the subscription renews, after the bill cluster drains the account, after the purchase creates a tight week, or after the extra payment leaves you short.

With Shelter, you find out earlier.

That earlier moment is where you have choices. You can wait, cancel, move, pause, transfer, downgrade, or simply spend with confidence because the money is truly safe.

That is the point of Shelter. Not a perfect budget. Not guilt. Not financial theater.

Just a clearer answer to the question that matters most day to day:

"What can I do with my money right now without hurting future me?"

Start with Shelter's safe-to-spend app, cash flow forecasting app, or pricing page if you want to see how the system fits together.

Take control of your cash flow

Shelter connects to your bank, forecasts your balance 30 days out, and alerts you before problems happen.