You have read the standard saving money advice a hundred times. Make coffee at home. Skip the avocado toast. Brown bag your lunch. And while there is nothing wrong with any of that, most of those tips save you a few dollars a day while ignoring the larger leaks in your budget that cost you hundreds per month.

This is a different kind of list. These are 15 saving money tips that real people actually use in 2026, organized by how much effort they require. Some take five minutes. Some take an afternoon. A few require a bigger decision. All of them work.

Quick Wins (15 Minutes or Less)

1. Audit Your Subscriptions

This is the single highest-return activity on this list relative to the time it takes. Pull up your bank statement, scan for recurring charges, and cancel everything you have not actively used in the last 30 days. The average person carries three to four subscriptions they have forgotten about or do not use. At $10 to $20 each, that is $30 to $80 per month back in your pocket.

If you want a thorough approach, the guide on zombie subscriptions costing you money walks through the full audit process including how to catch the sneaky ones like annual charges and free trials that converted.

2. Switch to Store Brands and Generics

For most grocery and household items, the generic version is manufactured in the same facility as the name brand. The difference is packaging and marketing, not quality. Switching your staples -- cereal, cleaning supplies, over-the-counter medication, canned goods, pantry basics -- to store brands typically saves 20-30% on your grocery bill without any noticeable quality difference.

Prescription medications are an even bigger opportunity. If you are paying for a brand-name drug, ask your pharmacist or doctor about the generic equivalent. The savings can be substantial.

3. Use Your Library

Your local library card is the most underutilized money-saving tool in existence. Beyond books, most libraries now offer digital borrowing through apps like Libby and Hoopla, giving you access to ebooks, audiobooks, magazines, movies, and music -- all free. Some libraries also offer passes to local museums, tool lending, and even mobile hotspots.

If you are currently paying for Audible, a newspaper subscription, or a magazine app, check your library's digital offerings first. You may be able to cancel one or more paid subscriptions.

4. Activate Your Cash Back

If you are using a debit card for everyday purchases, you are leaving money on the table. A basic no-annual-fee cash back credit card returns 1-2% on everything you buy, and some offer 3-5% in rotating categories. On $2,000 in monthly spending, that is $20 to $40 per month, or $240 to $480 per year.

The catch: this only works if you pay the balance in full every month. If you carry a balance, the interest will vastly exceed the cash back. If credit cards are a spending trigger for you, skip this tip entirely. The risk is not worth it.

Medium Effort (An Afternoon)

5. Meal Prep One Day Per Week

Eating out and ordering delivery are among the biggest discretionary expenses in most household budgets. You do not need to stop entirely -- that is not realistic or enjoyable. But replacing three or four takeout meals per week with home-cooked food saves $40 to $80 per week for most households.

Meal prepping on Sunday for the first half of the week eliminates the daily "what is for dinner" decision that often ends with opening a delivery app. Cook two or three large batches, portion them out, and reheat during the week. It does not have to be complicated or gourmet. It just has to be ready.

6. Do an Energy Audit

Your utility bills are a recurring expense you can reduce without changing your lifestyle. Start with the obvious: LED bulbs (if you have not already switched), a programmable thermostat, sealing drafts around windows and doors, and adjusting your water heater temperature to 120 degrees.

Many utility companies offer free home energy audits. They will send someone to your house, identify where you are wasting energy, and often provide free or discounted improvements. A few hours of effort can cut your monthly utility bill by 10-20% permanently.

7. Negotiate Your Bills

Call your internet provider, insurance company, and cell phone carrier. Tell them you are considering switching to a competitor and ask if they have any promotions or loyalty discounts. This works more often than you would expect. Companies spend far more to acquire new customers than to retain existing ones, so they have retention offers available that they will not mention unless you ask.

Do this once a year. The calls take 20 to 30 minutes each, and the savings can be $20 to $50 per month per provider. If you dislike phone negotiations, services like Trim or Rocket Money will do it for you in exchange for a percentage of the savings.

For a comprehensive approach to lowering your fixed costs, the guide on how to reduce monthly bills covers negotiation scripts and strategies.

8. Carpool or Optimize Your Commute

Gas, maintenance, insurance, and depreciation make your car one of the most expensive things you own. Any reduction in driving saves money across all four categories. Carpooling with a coworker, combining errands into fewer trips, or using public transit even part-time can reduce your transportation costs significantly.

If remote work is an option for even one or two days per week, the savings extend beyond gas to include wear on your vehicle, reduced parking costs, and fewer lunches bought near the office.

Bigger Moves (Require a Decision)

9. Refinance High-Interest Debt

If you are carrying a credit card balance, a personal loan, or a car loan with a high interest rate, refinancing or consolidating at a lower rate saves money every month for the remaining life of the loan. A balance transfer to a 0% APR credit card, a debt consolidation loan, or simply calling your credit card company to ask for a rate reduction can all reduce what you are paying in interest.

This is not about taking on more debt. It is about paying less for the debt you already have. The math is straightforward: reducing a $5,000 credit card balance from 24% APR to 12% APR saves roughly $50 per month in interest alone.

10. House Hack

If you own a home or rent a larger space than you need, using part of it to generate income is one of the most impactful financial moves available. Renting a spare room, listing a basement suite on Airbnb, or renting out a parking spot in a city where parking is scarce can offset a significant portion of your housing costs.

This is not for everyone -- it depends on your living situation, local regulations, and personal comfort level. But for those in a position to do it, the impact on monthly savings is often larger than all the other tips on this list combined.

11. Develop a Side Income Stream

This is not the "hustle culture" advice to work 80 hours a week. It is the recognition that the most effective way to save more money is often to earn more money. A modest side income of $300 to $500 per month, directed entirely to savings, builds an emergency fund in months instead of years.

The best side income leverages skills you already have: freelance writing, tutoring, photography, web design, consulting, teaching a class, selling crafts. The key is to keep it sustainable and to direct the income to savings before it gets absorbed into regular spending.

12. Automate Your Savings

If you are relying on willpower to transfer money to savings each month, you are fighting a losing battle. Set up an automatic transfer that runs on payday, even if it is a small amount. The automation removes the decision, and the consistency builds over time.

The full breakdown of how to set this up, including timing, amounts, and common mistakes, is in the guide on how to automate your savings.

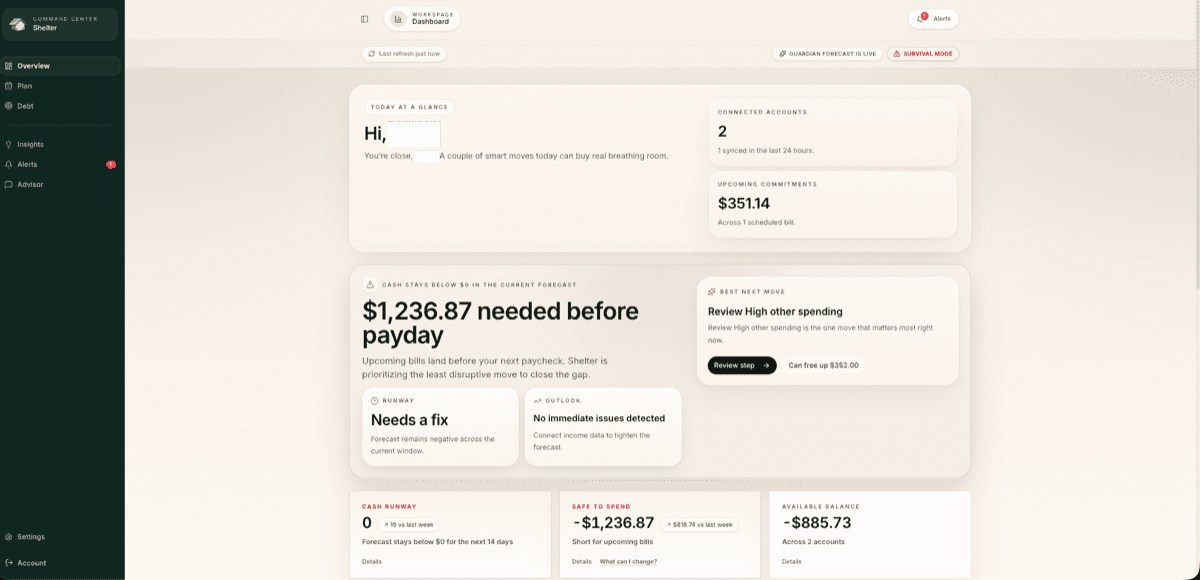

13. Use Cash Flow Tools Instead of Budgets

Traditional budgets fail for most people because they require constant tracking and categorization. Cash flow tools take a different approach: they show you what is coming in and going out over the next 30 days, so you can see exactly when you have room to save and when you need to hold back.

You can try Shelter's demo to see what this looks like. By connecting to your bank and analyzing your transaction patterns, it shows your projected balance for every day of the upcoming month. That visibility makes it obvious when extra money is available to move to savings and when it needs to stay put.

14. Downsize One Thing

Pick the single largest discretionary expense in your life and downsize it. Not eliminate -- downsize. If you have a premium cable package, switch to a basic streaming plan. If you drive a car with a $500 monthly payment, consider whether your next car could be a $250 payment. If you eat out four nights a week, try two.

The savings from downsizing one large expense often exceeds the combined savings from dozens of small frugality tips. A $200 per month reduction in your car payment saves $2,400 per year. That is a lot of homemade coffee.

15. Use the 30-Day Purchase Rule

For any non-essential purchase over $50 (adjust this threshold to your income level), wait 30 days before buying. Add it to a list, note the date, and revisit it a month later. If you still want it and can afford it, buy it. If you have forgotten about it or the desire has faded, skip it.

This rule eliminates impulse purchases, which are one of the largest drains on household budgets. The temporary desire that drives an impulse buy almost always fades. The money you did not spend is still in your account.

Making It Stick

The tips that work are the ones you actually do, consistently. Picking three or four from this list and committing to them will save more money over a year than trying all fifteen and abandoning most of them after a week.

Start with the quick wins. Audit your subscriptions and switch to store brands today. Those take almost no effort and produce immediate, recurring savings. Then pick one medium-effort and one bigger-move tip to implement over the next month.

The goal is not to live a life of deprivation. It is to plug the leaks that drain your money without adding anything to your life, and redirect that money toward things that actually matter to you -- whether that is an emergency fund, a vacation, debt freedom, or just the peace of mind that comes from knowing you have a cushion.

Take control of your cash flow

Shelter connects to your bank, forecasts your balance 30 days out, and alerts you before problems happen.