Most people who struggle with debt do not have an information problem. They know they should pay more than the minimum. They know interest is working against them. What they lack is a plan that survives contact with real life -- one that accounts for irregular income, unexpected expenses, and the very human tendency to lose motivation after a few months.

This guide is about building that plan. Not a theoretical exercise on a spreadsheet, but a system that fits into the way you actually spend and earn money.

Step 1: List Every Debt You Owe

Get everything on paper, or on a screen. Every credit card, every loan, every medical bill, every "I'll pay you back" that turned into a formal arrangement. For each one, write down:

- Creditor name

- Current balance

- Interest rate (APR)

- Minimum monthly payment

- Due date

Here is an example of what this might look like:

| Debt | Balance | APR | Minimum | Due Date |

|---|---|---|---|---|

| Visa card | $4,200 | 22.9% | $84 | 15th |

| Medical bill | $1,800 | 0% | $75 | 1st |

| Car loan | $9,500 | 5.9% | $225 | 20th |

| Student loan | $18,000 | 5.5% | $190 | 28th |

Total debt: $33,500. Total minimum payments: $574/month.

Seeing it all in one place can be uncomfortable, but it is the foundation everything else builds on. You cannot make a realistic plan for a number you are guessing at.

Step 2: Figure Out What You Can Actually Pay

Your debt payoff plan lives inside your cash flow. If you commit to paying $800/month toward debt but your actual available cash after bills and groceries is $650, the plan will break within weeks.

Start with your take-home pay. Subtract your non-negotiable expenses: rent or mortgage, utilities, groceries, insurance, transportation. What is left is your available cash for debt payments, savings, and discretionary spending.

Be honest with yourself here. If you budget $200/month for food and you actually spend $400, the plan needs to use $400. A plan built on aspirational numbers is not a plan -- it is a wish.

If you are not sure where your money goes each month, connect your bank account to Shelter and look at 30 days of actual spending. Shelter pulls in your real transactions and forecasts your cash flow forward, so you can see exactly how much room you have for debt payments without putting yourself in a hole.

Step 3: Set a Realistic Timeline

Now you have two numbers: your total debt and your monthly available cash for extra payments (above minimums). These two numbers define your timeline.

Using the example above, say you have $300/month available above your minimums. That means you are putting $874/month toward debt ($574 in minimums plus $300 extra).

At that pace, here is a rough timeline depending on which debts you target first:

- Medical bill first (snowball approach): The $1,800 medical bill is gone in about 6 months. Then you have $375/month extra for the next target.

- Visa card first (avalanche approach): The 22.9% credit card gets paid down aggressively. It takes about 10 months, but you save more in interest over the life of the plan.

Either way, with consistent payments, all four debts in this example can be paid off in roughly 3 to 4 years. That feels long right now, but it is a concrete number you can work toward.

For a detailed comparison of the snowball and avalanche methods, see debt snowball vs. avalanche.

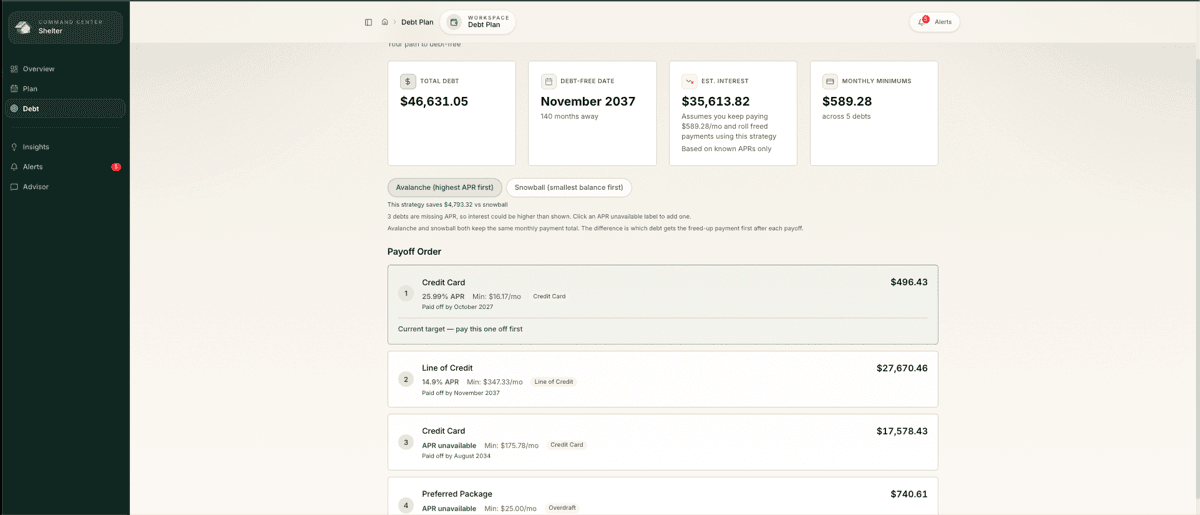

Step 4: Choose Your Method and Order Your Debts

Once you have decided on snowball, avalanche, or a hybrid approach, put your debts in order. This is your payoff sequence. Write it down somewhere you will see it regularly.

Using the avalanche method on our example:

- Visa card -- $4,200 at 22.9%

- Car loan -- $9,500 at 5.9%

- Student loan -- $18,000 at 5.5%

- Medical bill -- $1,800 at 0%

Every month, pay the minimum on debts 2 through 4 and put everything else toward debt 1. When debt 1 is gone, its entire payment rolls into debt 2. And so on.

Step 5: Build It Into Your Cash Flow

A plan that exists only on a spreadsheet will not survive. It needs to be embedded in how your money actually moves.

Automate your minimum payments. Set up autopay for every debt. This prevents late fees and protects your credit score. Schedule them a day or two after your paycheck hits.

Automate your extra payment. Set up a recurring transfer or payment for your extra amount on the same day. If you get paid biweekly, split the extra payment in half and make it biweekly too.

Use your cash flow forecast. Months are not all the same. Some months have three paychecks. Some months have car insurance renewals or annual subscriptions. Looking at your cash flow 30 days ahead lets you adjust -- you might pay $400 extra one month and $200 the next, and that is perfectly fine. What matters is the long-term average.

This is where a tool like Shelter is particularly useful. It connects to your bank, sees your recurring bills and income, and shows you what your balance will look like 30 days from now. You can see, in real numbers, whether that $300 extra payment this month will leave you comfortable or tight.

For more on the paycheck-to-paycheck angle, see paycheck-to-paycheck cash flow planning.

Step 6: Set Milestones and Track Them

A 3 to 4 year plan needs checkpoints. Without them, the grind wears you down. Here are milestones worth tracking:

- First debt eliminated. This is the biggest psychological win. Mark the date, notice how it feels.

- 50% of debts paid off by count. Two of four debts gone. You are past the halfway mark in terms of accounts.

- 50% of total balance paid off. When your total remaining debt drops below half of where you started, that is meaningful progress.

- Under $10,000 remaining. If you started with $33,500, seeing a number below $10,000 tells you the end is close.

- Final payment. The one you have been waiting for.

Write these milestones down. When you hit one, acknowledge it. You do not need to throw a party, but you should at least pause and recognize what you did. Progress you do not notice is progress that does not motivate you.

Step 7: Plan for Setbacks

Your car will need a repair. You will have an unexpected medical expense. Something will happen that was not in the plan. This is not failure; it is life.

Build a setback protocol into your plan before you need it:

For small setbacks (under $500): Reduce your extra debt payment for one month and cover the expense from cash flow. Resume normal payments next month.

For medium setbacks ($500 to $2,000): Pause extra payments entirely for one to two months. Pay minimums only. Cover the expense. Get back on track when you can.

For large setbacks (over $2,000): This is why emergency funds matter. If you do not have one, you may need to put the expense on a card and add it to your payoff plan. Adjust your timeline, but do not abandon the plan.

The plan is not fragile. Missing one month of extra payments adds a month to your timeline. It does not erase the progress you have already made.

Step 8: Celebrate Wins Along the Way

Debt payoff advice tends to be aggressively spartan: cut everything, spend nothing, suffer until it is over. That approach works for about six weeks before most people burn out.

Build small rewards into your plan. When you pay off a debt, take yourself out to dinner. When you hit the 50% milestone, buy something you have been wanting that costs less than one month's extra payment. The key word is "small." You are not undoing your progress; you are maintaining your sanity.

The people who successfully pay off large amounts of debt are not the ones who white-knuckled their way through three years of deprivation. They are the ones who built a sustainable rhythm that included enough joy to keep going.

Step 9: Reassess Every Quarter

Every three months, spend 15 minutes reviewing your plan:

- Are you ahead of schedule or behind?

- Has your income changed?

- Have any interest rates changed (variable rate loans, new promotional offers)?

- Is your payoff order still optimal?

Life changes, and your plan should change with it. A raise at work means more money for debt. A job loss means you might need to pause. A balance transfer offer at 0% might change which debt you should target next.

Getting Started Today

You do not need to have every detail figured out before you begin. Start with step 1: list your debts. Then figure out your available cash. Then pick a method. The plan will get more refined as you go, but the most important thing is that it exists and that you are following it.

If you want help seeing the full picture -- your income, your bills, your debts, and your cash flow all in one place -- connect your accounts through Shelter. When you can see 30 days ahead, building a debt payoff plan stops being abstract and starts being something you can actually act on.

Also check out how to pay off credit card debt for specific strategies on tackling high-interest card balances, which are often the first target in any debt payoff plan.

The plan does not need to be perfect. It needs to exist, and you need to follow it. Start today.

Take control of your cash flow

Shelter connects to your bank, forecasts your balance 30 days out, and alerts you before problems happen.