Personal finance apps have gone through three distinct eras. The first was manual entry: you opened an app, typed in your purchases, and categorized them by hand. It worked, if you had the discipline to do it every single day. Most people did not.

The second era was automatic sync. Apps like Mint connected to your bank accounts, pulled in transactions, and categorized them for you. This was a major step forward. No more manual entry. But the core experience was still backward-looking -- you got charts showing where your money went, which was interesting but not always actionable.

Now we are entering the third era. AI-powered apps that do not just show you the past but predict the future, spot problems before they happen, and give you personalized guidance based on your actual data. This is the era where finance apps go from reporting tools to something closer to actual advisors.

Here is what is changing and what to look for as this shift accelerates.

From Tracking to Predicting

The biggest shift in personal finance technology is the move from backward-looking tracking to forward-looking prediction.

Traditional apps tell you: "Last month you spent $420 on groceries." That information is mildly useful for planning next month, but it does not help you in the moment. It does not warn you that your account balance is going to dip below $50 on the 14th because three bills are drafting the same day.

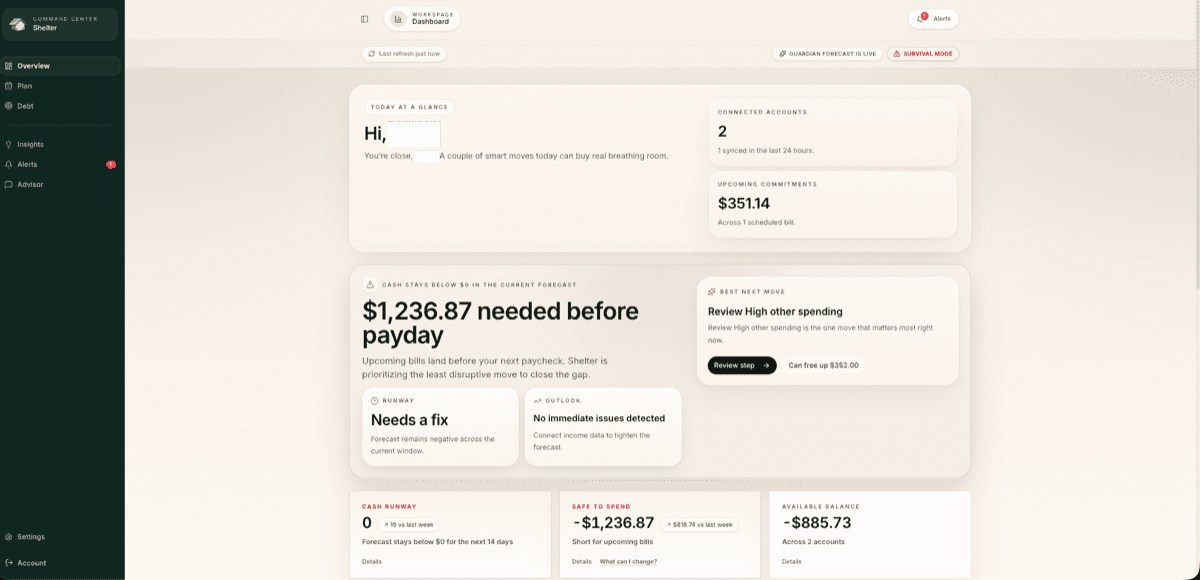

The new generation of apps uses machine learning to analyze your transaction patterns and project your future balance. They see that your rent hits on the 1st, your car payment on the 10th, your paycheck on the 15th, and your average daily spending is $35. They layer these patterns onto a timeline and show you what the next 30 days look like.

This capability -- cash flow forecasting -- is the feature that most clearly separates the next generation of finance apps from the previous one. It transforms the fundamental question from "What happened to my money?" to "What is going to happen to my money?"

Conversational AI

The second major trend is the integration of conversational AI into finance apps. Instead of clicking through menus and charts to find information, you ask questions in plain language and get answers.

"How much did I spend on food this week?" "Am I on track to make it to payday?" "What subscriptions am I paying for that I have not used lately?" These questions should be answerable instantly, in natural language, without requiring you to navigate to a specific screen and interpret a chart.

This is not a gimmick. The reason most people do not engage with their finance apps is that extracting useful information takes too much effort. You have to know which screen to look at, what time period to select, and how to interpret the data. Conversational interfaces eliminate that friction. You ask what you want to know, and you get a direct answer.

The quality of conversational AI in finance varies enormously. Some apps have little more than a keyword-matching system that redirects you to FAQ articles. Others have genuine AI that understands context, remembers your previous questions, and can analyze your actual financial data to give personalized answers. The difference is significant, and it is worth testing before you commit to any app.

Proactive Alerts

Related to prediction is the move toward proactive alerts. Instead of waiting for you to open the app, it reaches out to you when something needs your attention.

The most valuable alerts are:

Cash crunch warnings. Your projected balance is going to drop below a safety threshold in the next week. You see this notification days in advance, not after an overdraft fee has already been charged.

Unusual charges. A transaction that does not match your typical pattern -- a charge from a merchant you do not recognize, a bill that came in significantly higher than usual, or a subscription you have not used in months.

Spending trend alerts. Your grocery spending this month is tracking 20% higher than your average. Your dining out is on pace to be double what it was last month. These trends are invisible in real-time but obvious in aggregate, and AI can flag them while there is still time to adjust.

Bill change notifications. A subscription increased its price. An insurance premium went up. Your phone bill is $15 higher than usual. These small changes often go unnoticed but add up over time.

The best proactive alerts are specific and actionable. "Your balance may be low" is vague. "Your balance will be approximately $43 on Thursday after your car payment drafts -- $287 lower than your average Thursday balance" is useful because it tells you exactly what the problem is and when it will happen.

The Read-Only Security Focus

A growing trend in finance apps is the emphasis on read-only access as a security feature rather than a limitation.

Early finance apps tried to do everything: track spending, pay bills, move money between accounts, invest spare change. Each additional capability required additional permissions and increased the attack surface. When an app can move your money, a security breach has direct financial consequences.

The newer approach is to keep finance apps strictly read-only. They connect to your bank accounts to see your data but cannot initiate any transactions. They cannot transfer money, pay bills, or change account settings. This means that even if someone compromised the app entirely, they could not take a single dollar from your accounts.

This is not just a technical decision. It reflects a philosophical shift in how finance apps think about their role. The app's job is to give you clarity and insight. Your bank's job is to hold and move your money. Keeping those roles separate is better for security and better for the user experience.

Shelter was designed around this principle from the start. It connects through Plaid with read-only access, which means it can analyze your transactions, predict your cash flow, and alert you to problems, but it never has the ability to touch your money. The read-only architecture is a core security feature, not a compromise. If you are comparing modern tools, the Rocket Money alternative and YNAB alternative pages show how Shelter is positioned differently.

What to Look for in a Finance App in 2026

Given these trends, here is what is worth prioritizing when choosing a personal finance app:

Forward-looking features over backward-looking reports. Charts of last month's spending are table stakes. Cash flow projections, balance forecasting, and predictive alerts are what actually help you make better decisions going forward.

AI that is personalized, not generic. An AI that says "you should save more" is a billboard, not an advisor. An AI that says "you have three subscriptions totaling $42 that you have not used in 60 days" is actually useful because it is based on your specific data.

Read-only bank connections. There is no good reason for a finance tracking and insights app to have write access to your bank accounts. If an app asks for the ability to initiate transactions, ask yourself why.

A sustainable business model. If the app is free, examine how it makes money. Ad-supported finance apps have an inherent conflict of interest. Data-selling models put your financial privacy at risk. Subscription models, where you pay a monthly fee and the company makes money by keeping you happy, tend to have the cleanest incentives.

Privacy-first data handling. Your financial data is among the most sensitive information you have. The app should encrypt it, should not sell it, and should give you control over what is shared. Check the privacy policy before you connect your bank accounts.

Where the Industry Is Heading

The trajectory of personal finance technology points toward increasingly autonomous financial management. Not autonomous in the sense that AI makes decisions for you, but autonomous in the sense that the monitoring, pattern recognition, and alerting happen without requiring your active involvement.

Today, you have to open your finance app to check on things. Tomorrow, the app will reach out to you only when something requires your attention. The default state will be "everything is fine, and here is proof." The exceptions -- a cash crunch approaching, an unusual charge, a bill increase -- will be surfaced proactively with enough context and lead time to act on them.

We are also moving toward AI that can handle increasingly nuanced financial questions. Not just "how much did I spend on groceries?" but "given my current spending trajectory, income, and bills, can I afford to take an unpaid week off next month without going below my $500 safety threshold?" These multi-variable questions currently require either a spreadsheet or a human advisor. AI is getting good enough to answer them in real time.

The biggest barrier to adoption remains trust. People are understandably cautious about giving any technology access to their financial data. The companies that win in this space will be the ones that earn trust through transparency, read-only access, clear privacy policies, and a business model that aligns their incentives with the user's interests.

The era of finance apps that just show you pie charts is ending. The era of apps that actually help you navigate your financial life in real time is beginning. If you want to see what this looks like in practice, the features page walks through how proactive finance management works, and how AI helps manage money covers the underlying capabilities that make it possible.

The right time to upgrade your financial tools is before you need them to bail you out of a problem. It is always cheaper to prevent a crisis than to recover from one, and the tools to do that are better now than they have ever been.

Take control of your cash flow

Shelter connects to your bank, forecasts your balance 30 days out, and alerts you before problems happen.