The question is not whether AI chatbots or human financial advisors are "better." They are built for different problems. Using an AI chatbot for estate planning is like using a calculator to write a novel. Using a human advisor to check whether you can afford lunch today is like hiring an architect to hang a picture frame.

The useful question is: when does each one make sense? And for most people, the answer involves using both at different stages and for different kinds of decisions.

What AI Chatbots Are Good At

AI financial chatbots excel at a specific category of tasks: frequent, data-intensive, low-stakes decisions that benefit from speed and always-on availability.

Daily Financial Decisions

"Can I afford to order dinner tonight, or should I cook?" "How much have I spent on coffee this month?" "Is my balance going to be okay until Friday?" These are the micro-decisions that happen every day and collectively have a huge impact on your financial health.

No human advisor is available -- or affordable -- for questions like these. But an AI chatbot connected to your bank data can answer them instantly, any time of day, based on your actual numbers rather than a guess.

Quick Pattern Spotting

An AI chatbot can scan months of transaction data in seconds and surface insights that would take you hours to find manually. "Your spending at restaurants is up 35% compared to the last three months." "You have been charged by a service called CloudSync Pro for the last four months but had never used it before August." "Your electric bill has increased every month since October."

These observations are not complex analysis. They are pattern matching at scale, which is exactly what AI is built for. A human advisor reviewing your bank statements would theoretically notice the same things, but the time and cost involved make it impractical for routine monitoring.

24/7 Availability

Financial anxiety does not operate on business hours. The worry about whether you can cover rent this month tends to hit at 2 AM, not during a scheduled appointment. An AI chatbot is available whenever the question arises, which means you get answers when you actually need them rather than days later when the anxiety has either resolved itself or festered.

Cash Flow Monitoring

Monitoring your cash flow is an ongoing, continuous task. Your balance changes every day. Bills draft at different times. Income arrives on its own schedule. Keeping track of all of this manually is tedious and error-prone.

AI handles continuous monitoring effortlessly. It watches your accounts, tracks patterns, and alerts you when something needs attention. This is not a task that benefits from human wisdom or emotional intelligence. It benefits from persistence and attention to detail, which are AI's core strengths.

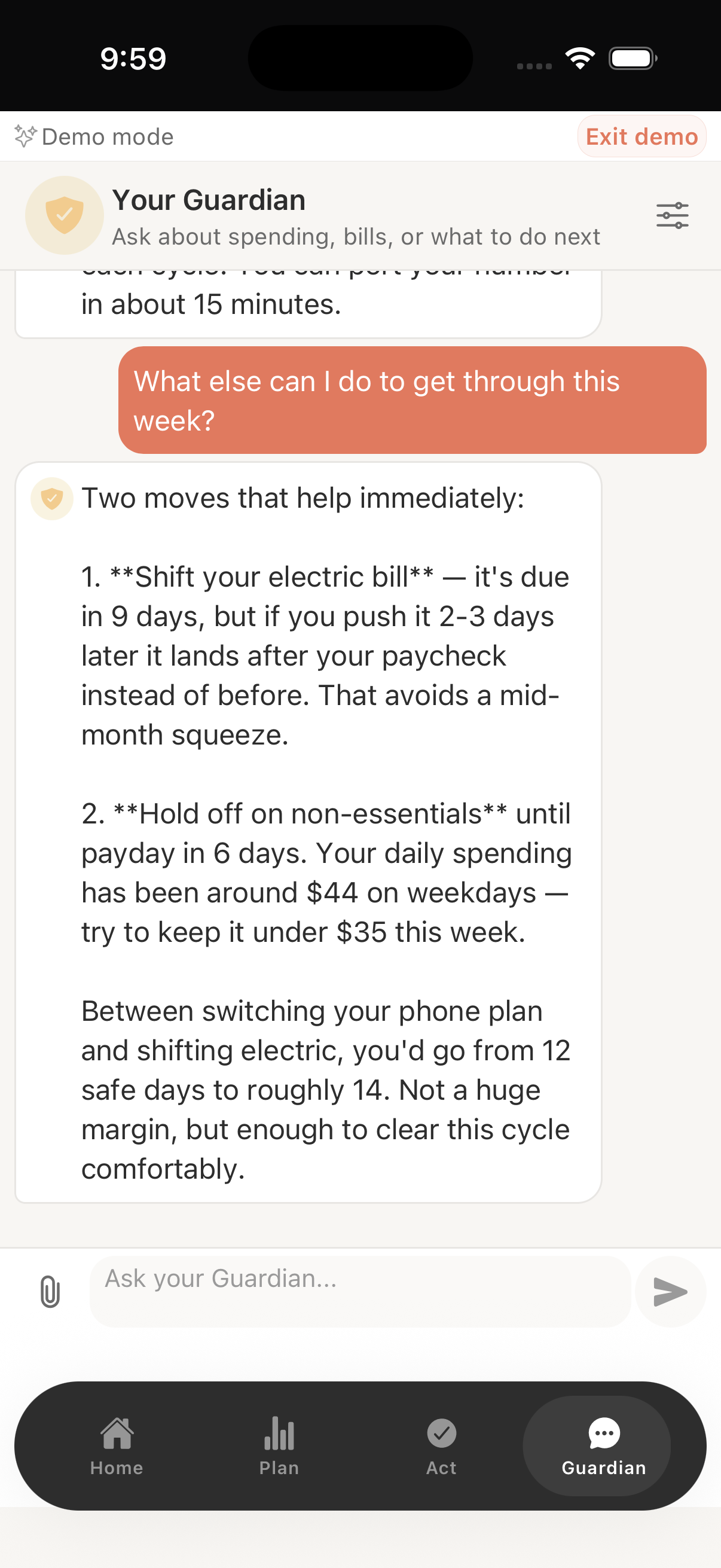

Shelter's Guardian is designed for exactly this kind of work. It monitors your accounts, answers questions about your spending and cash flow, and alerts you when something unusual happens or when a cash crunch is approaching. You can see how it works in the demo.

What Human Advisors Are Good At

Human financial advisors bring capabilities that AI fundamentally lacks: judgment born from experience, emotional intelligence, and the ability to navigate complex, ambiguous situations where the "right" answer depends on values and priorities that cannot be reduced to data.

Complex Tax Planning

Tax strategy across multiple income sources, business entities, investment accounts, and life changes is genuinely complex. Deciding between a Roth conversion and a traditional IRA contribution involves projecting future tax rates, estimating retirement income, considering estate implications, and weighing legislative risk. This is where human expertise earns its fee many times over.

AI can handle basic tax questions. But when your situation involves a rental property, a side business, stock options from your employer, and a spouse with their own financial complexity, you need a human who can see the full picture and make judgment calls.

Estate Planning

Wills, trusts, beneficiary designations, powers of attorney -- these are legal documents with real consequences that vary by state and family situation. A mistake in estate planning can cost your heirs tens or hundreds of thousands of dollars. This is not a domain where "pretty good" AI advice is acceptable.

Emotional Coaching

Money is emotional. The decision to sell investments during a market crash is not a math problem. It is a fear management problem. The choice between paying off your mortgage early (mathematically suboptimal at low interest rates) or having the peace of mind of owning your home outright is not a calculation. It is a values decision.

Human advisors who are good at their jobs function partly as coaches. They talk you off ledges, help you see past short-term emotions, and remind you of the plan you made when you were thinking clearly. AI cannot do this. It can tell you that selling your investments during a downturn is historically a bad idea, but it cannot look you in the eye and ask what is really driving the urge to sell.

Life Transitions

Getting married, having a child, getting divorced, losing a spouse, inheriting money, selling a business, retiring -- these transitions involve financial decisions that are deeply intertwined with emotions, relationships, and identity. A human advisor who understands your full context can guide you through these transitions in a way that AI cannot.

Cost Comparison

The cost difference between AI and human advice is significant and worth being explicit about.

AI chatbots are typically included in a finance app subscription, ranging from free to $10 to $15 per month. For that cost, you get unlimited access to daily financial guidance, monitoring, and answers to routine questions.

Human financial advisors come in several pricing models:

- Assets Under Management (AUM): Typically 0.5% to 1% of your portfolio annually. On a $200,000 portfolio, that is $1,000 to $2,000 per year.

- Fee-only (hourly): $150 to $400 per hour, depending on the advisor's experience and location.

- Fee-only (flat annual retainer): $2,000 to $7,500 per year for ongoing planning.

- Commission-based: The advisor earns commissions on products they sell you. This model has inherent conflicts of interest and is generally best avoided.

For routine daily money management, the cost of a human advisor is wildly disproportionate to the value. For complex planning that could save you tens of thousands in taxes or protect millions in estate value, the advisor's fee is a rounding error.

The Hybrid Approach

The most effective financial strategy for most people is using both: an AI chatbot for daily management and a human advisor for major decisions.

Here is what that looks like in practice:

Daily and weekly: Use an AI tool to monitor your cash flow, answer quick financial questions, catch unusual charges, and get alerts about upcoming bills or potential cash crunches. This is the operational layer of your finances.

Quarterly or annually: Meet with a human advisor to review your broader financial plan. Discuss tax strategy, investment allocation, insurance needs, and progress toward long-term goals. This is the strategic layer.

During life transitions: Engage a human advisor (or increase the frequency of meetings) when something major changes: job change, marriage, home purchase, business decision, inheritance. These are the moments where the cost of bad advice is highest and the value of human judgment is greatest.

The AI handles the volume. The human handles the complexity. Neither one does the other's job well.

When to Upgrade to Human Advice

If you have been managing your finances with apps and AI tools and things are going well, there is no urgent need to hire a human advisor. But certain signals suggest it is time:

Your tax situation has become complicated. Multiple income sources, investment properties, business income, or stock compensation all benefit from professional tax planning.

You have accumulated significant assets. Once your investment portfolio crosses $100,000 to $200,000, the impact of good (or bad) asset allocation becomes large enough to justify advisory fees.

You are approaching a major life change. Retirement planning, in particular, involves enough variables and enough at stake that professional guidance is worth the cost.

You are making a decision that is hard to reverse. Buying a house, funding a child's education, choosing between pension options -- these are one-way doors where the stakes justify expert input.

You feel overwhelmed. If financial complexity is causing you stress or paralysis, a human advisor can simplify things and give you a clear plan to follow. The psychological value of "someone competent is helping me with this" should not be underestimated.

Getting the Most From Both

To get the most from an AI chatbot, give it the best possible data. Connect all your accounts, not just one. The more complete the picture, the more accurate the insights. Ask it questions regularly so you build a habit of engagement. And pay attention to its alerts -- they are only useful if you act on them.

To get the most from a human advisor, come prepared. Before each meeting, review your financial situation, write down your questions, and be honest about your goals and concerns. The more context you give, the better the advice you get back. And ask about their credentials and compensation model before you hire them. A fee-only fiduciary is the gold standard.

The best financial outcome comes from neither AI nor human advice alone. It comes from using the right tool for the right job, at the right time. For a deeper dive into what AI financial advisors can and cannot do, or to understand how AI is changing money management more broadly, those articles go into the specifics.

Take control of your cash flow

Shelter connects to your bank, forecasts your balance 30 days out, and alerts you before problems happen.